How can I avail of the Home Renovation Incentive (HRI) Scheme?

The Incentive provides for tax relief by way of an Income Tax credit at 13.5% of qualifying expenditure on repair, renovation or improvement works carried out on a main home or rental property by qualifying Contractors.

The works must cost a minimum of €4,405 (before VAT) per property, which will attract a credit of €595 per property. Where the cost of the works exceeds €30,000 (before VAT) per property, a maximum credit of €4,050 per property will apply.

The credit is payable over the two years following the year in which the work is carried out and paid for. The first year for HRI tax credits is 2015 for Homeowners and 2016 for Landlords. The works must be carried out before 31 December 2016.

See further information on the link below:

http://www.revenue.ie/en/tax/it/reliefs/hri/

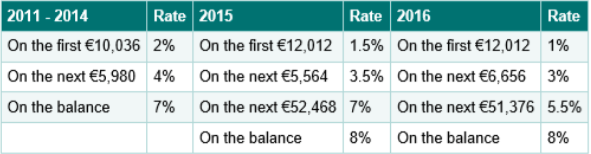

Please explain the new rates & exemptions for Universal Social Charge (USC).

The Exempt categories for Universal Social Charge for 2016 are:

- Where an individual’s total income for a year does not exceed €13,000

- All Department of Social Protection payments

- Income already subjected to DIRT

The standard rates of Universal Social Charge are:

See further information on the link below:

http://www.revenue.ie/en/tax/usc/

How does the new eTax Clearance system work?

eTax Clearance is available to business, PAYE and non-resident customers with a PPSN/Reference number. Customers who are tax compliant receive a Tax Clearance Access Number, which along with their PPSN/Reference number they give to a third party to verify their tax clearance details.

Tax clearance will be regularly reviewed and if a customer becomes non-compliant, their electronic tax clearance certificate can be withdrawn.

See further information on the link below:

http://www.revenue.ie/en/online/tax-clearance.html

What rate should my business re-imburse employees for kilometers travelled for business purposes?

Revenue provide a guideline for actual costs incurred which we have outlined below summarised as the Civil Service kilometric rates for cars, motorcycles and bicycles for individuals who are obliged to use their car, motorcycle or bicycle in the performance of the duties of their employment.

The Civil Service Rates for motor vehicles:

See further information on the link below:

http://www.revenue.ie/en/tax/it/leaflets/it51.html

Who qualifies for the Home Carer Tax Credit & what is the tax credit for 2016?

A tax credit at the standard rate of tax (20%) is available for Married Couples or Civil Partners where:

- One Spouse or Civil Partner (the ‘home carer’) works in the home, caring for one or more dependent persons (who usually live with the couple for the year).

- The couple in a marriage or civil partnership – must be jointly assessed to tax – it does not apply where couples are taxed as single persons.

- Home Carer’s income must not exceed €7,200 for the tax year.

The maximum credit per claim has increased from €810 in 2015 to €1,000 in 2016.

See further information on the link below:

http://www.revenue.ie/en/tax/it/credits/home-carers.html

Please explain the new tax credit available to self-employed individuals for 2016?

A new Earned Income Tax Credit of up to €550 was introduced for taxpayers earning self-employed trading or professional income in certain cases and to business owner/managers who are not eligible for a PAYE credit on their salary income. The tax credit will be calculated at 20% of a person’s earned income (excluding earned income that is taken into account for the PAYE Tax Credit) subject to a maximum of €550. Where an individual has earned income that qualifies for Earned Income Tax Credit and PAYE Tax Credit, the combined tax credits cannot exceed 1,650.

How can an unregistered farmer claim a VAT refund on farm buildings or structures, land drainage or land reclamation?

Revenue provide a Form VAT 58 – Claim by Unregistered Farmer for Refund of Value-Added Tax (VAT) under the Value Added Tax (Refund of Tax) (Flat Rate Farmers) Order 2012. This claim relates to construction, extension, alteration or reconstruction of farm buildings and structures or on land drainage and land reclamation.

VAT is not refundable on:

- repairs to farm buildings, structures and farm roadways

- outlay on roadways to dwelling house

- mobile equipment and machinery

- repair, service and maintenance of equipment and machinery

- ESB supply

- fuel, oil, diesel

Applications for repayment must be submitted within four years from the end of the taxable period to which the claim relates.

Original invoices supporting the VAT claim must be submitted to revenue.

See further information on the link below: http://www.revenue.ie/en/tax/vat/refunds/repayments-unregistered-persons.html#section4